NVDA post-market reaction (-7%) highlights the valuation problem. The correction of the tech sector should resume

NVDA 2Q beat consensus, 3Q guidance beat consensus, the stock declined post-market.

Overall, growth in Tech is mediocre (PC, smartphone, enterprise, telcos), with growth concentrated in AI Semis and Hyperscalers

The Tech segment of the NASDAQ 100 is expensive, Non-Tech is not.

As we get ready for the September quarter results, as the Tech sector (stock prices) is behaving a bit erratically, let’s take a step aside.

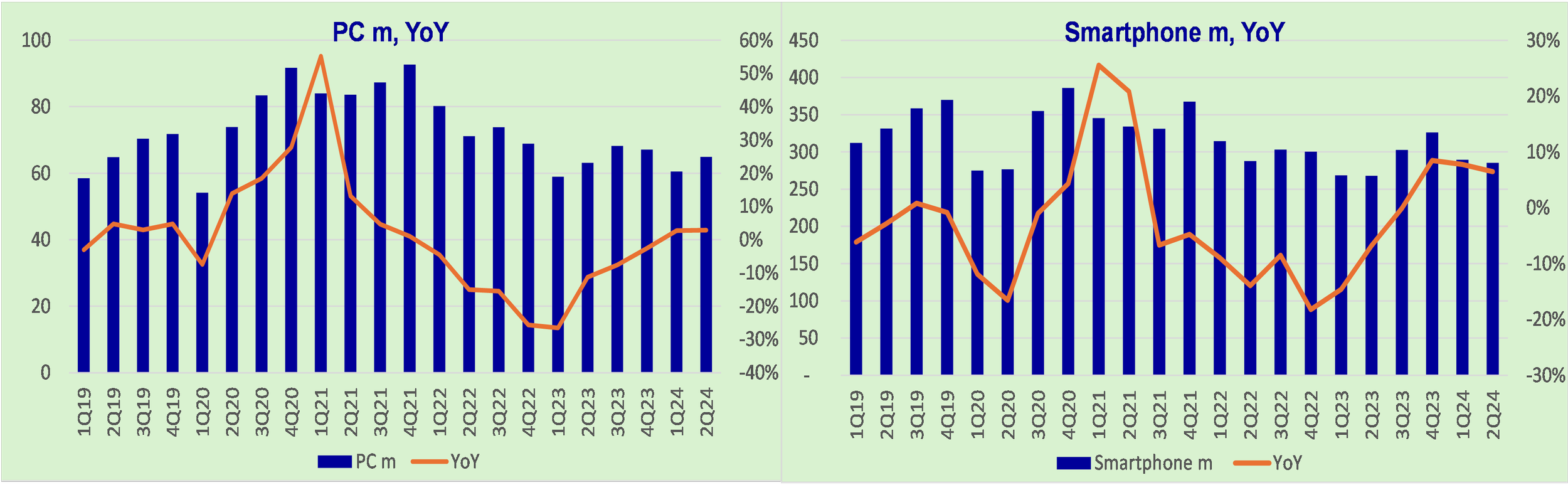

The main segments of end-demand aren’t doing great

PC units growing at 3% YoY (excess inventories were depleted end 2023, a bit of restocking in 1H24, now done).

Smartphone units growing at 6% YoY. Both Mediatek and Qualcomm mentioned that the smartphone market is flat to up low-single-digit in 2024. However, upgrades continue: 5G penetration up 10 points to 60% in 2024, AI-enabled phones doubling this year (the processor is 20-30% more expensive). So there is a good mix story for MTK and QCOM.

PC and Smartphone units, m, YoY

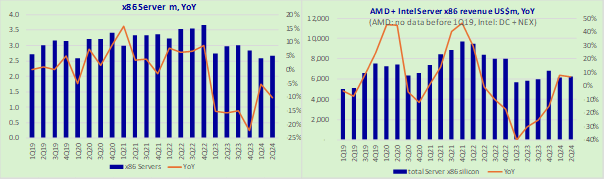

Enterprise. Traditional x86 Servers are flat in 2024. TrendForce forecasts +2%, my checks with Server assemblers in Taiwan points to a low-single-digit decline. Note that AMD and Intel’s x86 Server revenues are doing a tad better at +7% YoY. This is due to a little bit of restocking after the horrendous 2022-23 destocking, plus new CPU launches. But again, nothing impressive here.

Server units (m, YoY) and x86 Server CPU revenues of AMD and Intel (US$m, YoY)

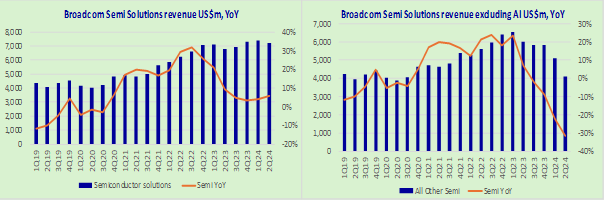

Another example is Broadcom. Since the firm now gives us AI revenue, we can calculate the non-AI Semi revenues – and that’s quite shocking. AI revenues are growing at ~300% YoY and All Others declining at -30% YoY. The declining components are listed below and are Enterprise / Telco related.

o Network switch / routers (excl AI) -50% YoY

o Broadband -30%

o Storage -27%

Broadcom Semiconductor revenues, AI included (left) and AI excluded (right)

Finally, as I wrote in early August, the Automotive / Industrial segment is still in correction mode.

Automotive and Industrial Semiconductor revenues US$m, YoY. Sum of ADI, Infineon, Microchip, NXP, ON Semi, Renesas, ST Micro, Texas Instruments.

The bright spots are few – but big

AI demand. NVDA. I won’t get into details other to say that NVDA 2Q results beat consensus (reported last night), 3Q revenue guidance beat consensus. And yet, post-market the stock declined -7%.

Broadcom, the other AI processor vendor reports tomorrow.

Hyperscalers. In aggregate, in 2Q24 Operating Profits increased 34% YoY, Net Income 2% YoY.

Sum of operating profits (left) and net income (right) for the sum of Amazon, Google, Meta, Microsoft - US$m, YoY

The problem remains valuations

I think that NVDA post-market reaction highlights the problem. Expectations are too high in some parts of the market, valuations are too high for the Tech sector, the macro / Feds / rate direction favors the old economy, small caps, etc and the rotation will continue.

To simplify, I downloaded NASDAQ100 stocks and separated them into

· Tech stocks: 41 in total. PEx is at + 1 standard deviation. The segment is trading at 28.3x 2025E versus average 24.5x

· Non-Tech stocks: 59. PEx is at the average. The segment is trading at 23.7x 2025E versus average 23.7x

Without further comments, the charts are explicit.

PEx valuations for the 41 Tech stocks in the Nasdaq100 (left) and the 59 Non-Tech stocks. 2025 earnings estimates from I/B/E/S.

Valuation table for Tech stocks Nasdaq100 and the Non-Tech stocks.